BIMCO has released an overview of the three main shipping sectors and their respective fleet growths so far this year taking into account the impact of the COVID-19 and other geopolitical developments on the global trade.

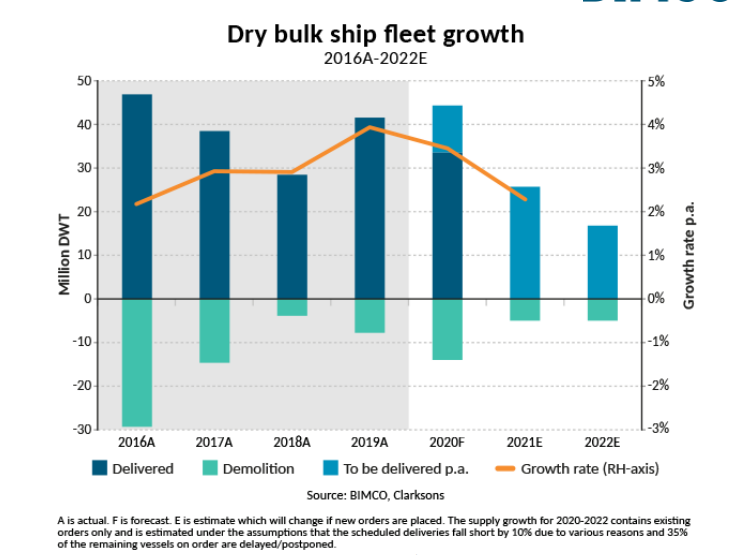

Bulkers

The dry bulk fleet has seen both deliveries and demolitions rise over the course of the pandemic while contracting has fallen steeply.

So far this year, the dry bulk fleet has grown by 2.8% and breached 900 million deadweight tonnes (DWT) for the first time. Currently, at 903.3 million DWT, BIMCO expects full-year growth to reach 3.5%.

On the other hand, the orderbook has fallen to 63.4 million DWT, its lowest level since April 2004. Deliveries have risen by 7.8 million DWT from this time last year, with 33.9 million DWT of new capacity arriving on the sea in the year to date.

Of this, just less than half of the tonnage comes from the 70 new Capesize ships that have been delivered (15.5 million DWT). Given that an average Capesize ship carries six loads a year, these new ships can carry 495 loads (200,000 tonnes) a year.

The 111 new Panamax ships will be able to carry an additional 893 loads (75,000 tonnes), as these average seven loads a year.

A sharp increase in fleet growth, as a result of these deliveries, has been somewhat offset by an increase in demolitions, but the fleet continues its growth, because even a 69.4% increase in demolitions, compared with last year, only amounts to 8.7 million DWT being demolished.

The pandemic and the poorer outlook have caused a 59.1% fall in contracting activity, as owners have not wanted to invest during a recession plagued by uncertainty. Only 108 new dry bulk ships have been ordered in 2020, totalling 7.5 million DWT, BIMCO’s data shows.

Of these, 10 are Capesize ships (210,000 DWT) all of which have been ordered by Chinese leasing interests. The most popular ship size has proven to be Handymaxes, of which 62 have been ordered, totalling 3.5 million DWT, the majority of which have a capacity of between 60,000 and 65,000 DWT.

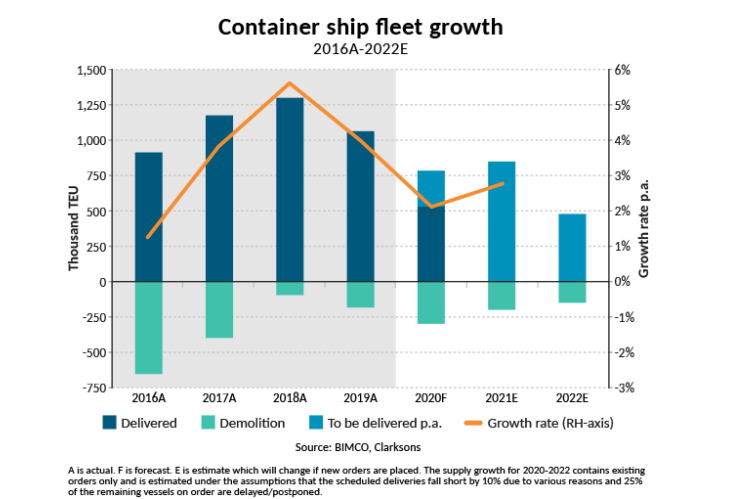

Containerships

The container shipping fleet has grown by 1.6% since the start of the year, reaching a total capacity of 23.2 million TEU. BIMCO expects that, over the whole year, the fleet will expand by 2.1%, which will mark a four-year low.

The association expects a total of 300,000 TEU to be demolished this year, so far this year 169,647 TEU have been demolished. The reopening of demolition yards on the Indian subcontinent, and the poor conditions in the container shipping charter market, saw owners pushed to getting rid of some of their older and substandard ships between June and August.

The youngest container ship to have been demolished this year was 15 years old. These newly demolished ships include some of the largest container ships ever to be demolished. At 9,600 TEU, the Sine Maersk (built 1998) is the largest container ship ever to be demolished.

“Though these used to be among the largest container ships sailing, they are now far outclassed by the latest deliveries, and given the cascading that has resulted in ever-larger ships on smaller trades, it has proven unattractive to keep these ships trading, even on the smaller trades,” BIMCO said.

So far this year, four ships above 6,000 TEU have been demolished. The pandemic has also greatly dampened the appetite for new ships; in the first eight months of this year, contracting activity has been 33.5% lower than last year, as only 162,834 TEU has been ordered.

This, combined with a normal pace of deliveries, has sent the container shipping orderbook to its lowest level since September 2003.

The share of the orderbook made up by Ultra Large Container Ships (ULCS 15,000+ TEU) has fallen below 50% (at 47.4%), as five new ULCS (all 23,000 TEU) have been ordered, while 13 have been delivered totalling 301,724 TEU. There are 927,296 TEU of ULCS on order as per early September.

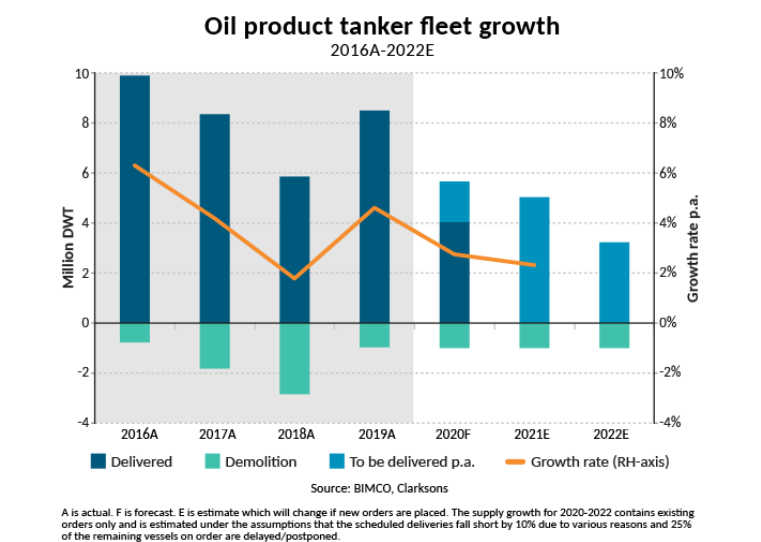

Tankers

In contrast to the other major shipping sectors, the crude oil tanker sector has seen very little demolition in the first six months of the year. In fact, only seven crude oil tankers were demolished in the first eight months of 2020, totalling 681,832 DWT.

Year to date, no VLCCs have been demolished, while 26 were delivered, resulting in the VLCC fleet growing by 7.9 million DWT. This is on top of the 68 VLCCs delivered in 2019, which led to the VLCC fleet growing by 8.6%. The last VLCC to be demolished was in June 2019, with only four having been demolished since October 2018.

BIMCO expects demolition activity to rise as freight rates and actual demand for tanker shipping falls, with total crude oil demolition coming to 7.5 million DWT in the full year and 1 million DWT of product tankers being demolished. So far this year, 547,334 DWT of oil-product tankers have been removed.

Over the full year, BIMCO expects that the oil product tanker fleet will grow by 2.7% and the crude oil tanker fleet by 2.4%. This represents a marked slowdown from last year, when they grew by 4.6% and 6.2% respectively. Total tanker deliveries have totalled 16.2 million DWT so far this year, a 43.9% drop from last year.

This slowdown in fleet growth will continue in the coming years, as the pandemic has lowered contracting activity. Contracting for crude oil tankers has fallen by 37.9% so far this year compared with last, BIMCO said.

At 4.1 million DWT, product tankers is the only segment in which there have been more new orders in the first eight months of this year than the same period of last year (+31.9%). Ten of these orders are for a series of 50,000 MR tankers placed by Bahri.

The lower contracting activity fits with the poorer outlook, which is also reflected in the value of second-hand tankers.

Prices for 10-year-old VLCCs and LR2s both fell by 19.2% and 18.4% respectively from the start of the year to late-August. A new VLCC is worth 7.5% less now than at the start of the year, and the value of an LR2 has fallen by 1.7% – drops of $7.35 million and $0.86 million respectively.

The post BIMCO: A look into 2020 fleet growth appeared first on Offshore Energy.